Tag Archives: money

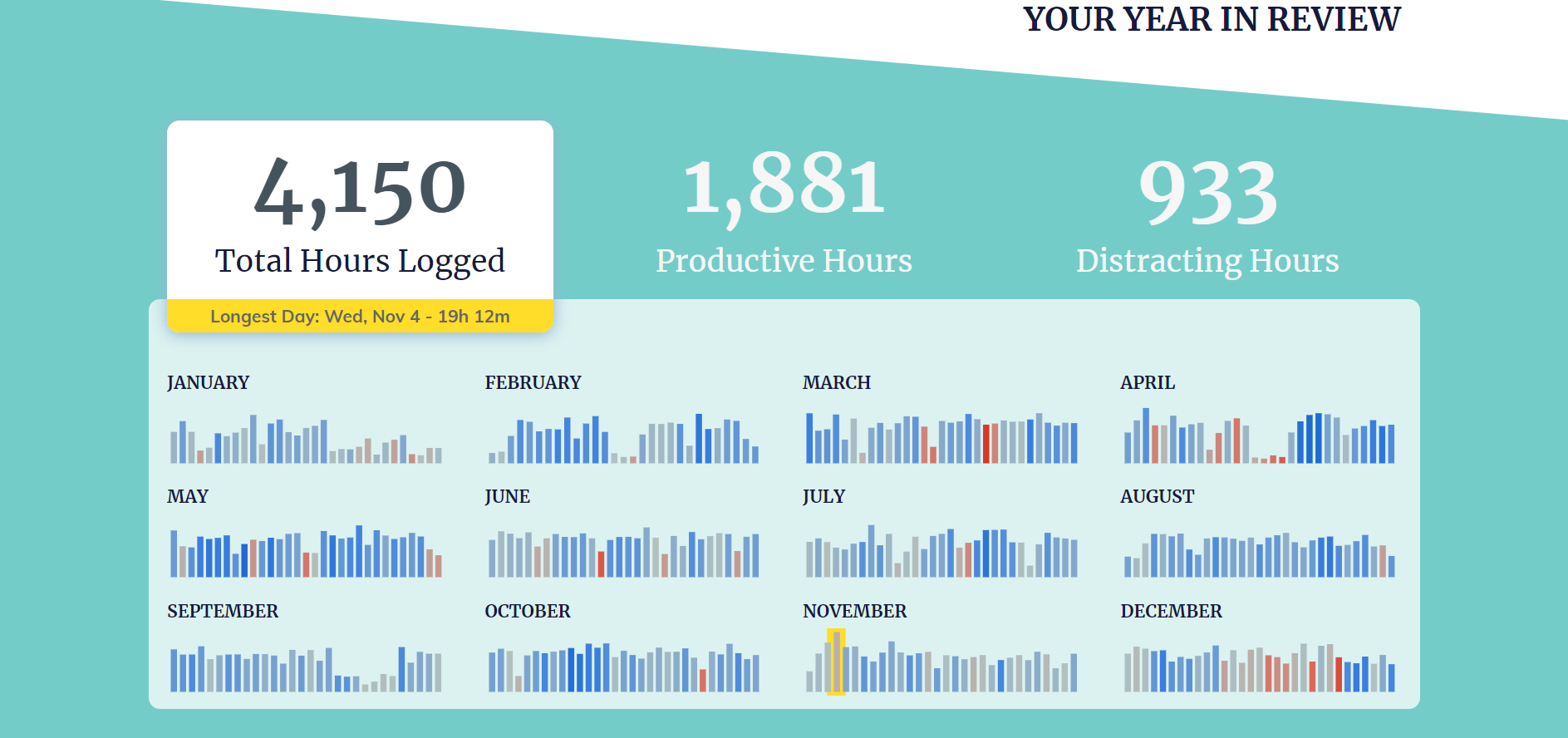

How To Track Your Whole Life

I’ve decided to write an accompanying piece to my end-of-year recap on how I track everything. Obviously, some people are not fans of being tracked, but I admit, I’m quite biased given I work in data, however; I think it’s a really good way to keep track of habits & re-prioritize your life, especially at the start of a new year!

Hey Christine, I Need Money Advice!

Sometimes people ask me for financial advice, so I thought this was a good time to put a quick how to together of how I went from having $9,000 in credit card debt to having a full year’s salary saved in 9 years.

Be Broke at 25 Not at 75: Why You Should Save Now

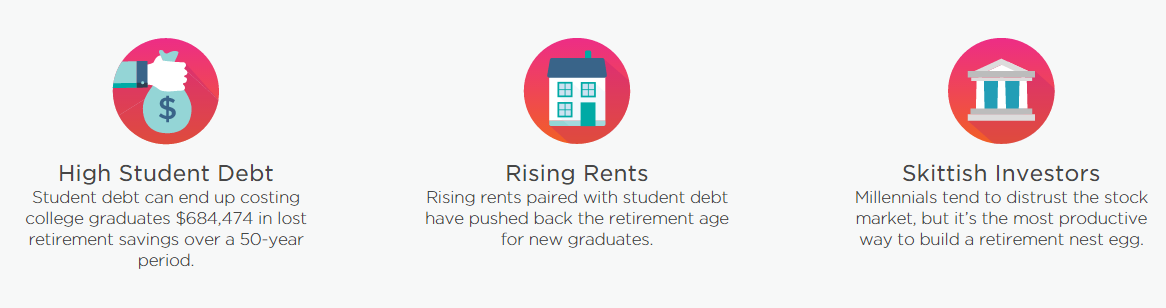

Nerdwallet just released a study that says “New Grads Won’t Be Able to Retire Until 75.” Yes, that means you. You will have to wait 50 years before you retire if you were fortunate enough to be born in the early 90s or late 80s. Why is that? Well, mostly student loans and high rent…

12 Money Questions We’re Not Asking Our Friends, But Should Be

I wouldn’t consider myself an open book, per say but the things that tend to be a big deal to others, usually weren’t to me. So then I thought, what are all the questions we’re not asking our friends & co-workers that we really should?

Asking for a Raise Template (MadLibs Style)

About a year after undergrad/getting my first real job, I emailed my bosses and asked for a raise. I asked for a 33% raise and ended up with a 25% raise.